Is your company now qualifying as a “Small Company” under the revised MCA limits?

- Expanded Eligibility: Companies with paid-up capital up to ₹10 crore and turnover up to ₹100 crore can now access small company benefits.

- Lower Compliance Burden: Significant relaxations in board meetings, filings, audit requirements, CSR, and penalties.

- Cost & Time Efficiency: Reduced professional certifications, simpler reporting, and lower statutory fees directly improve governance efficiency.

Scope

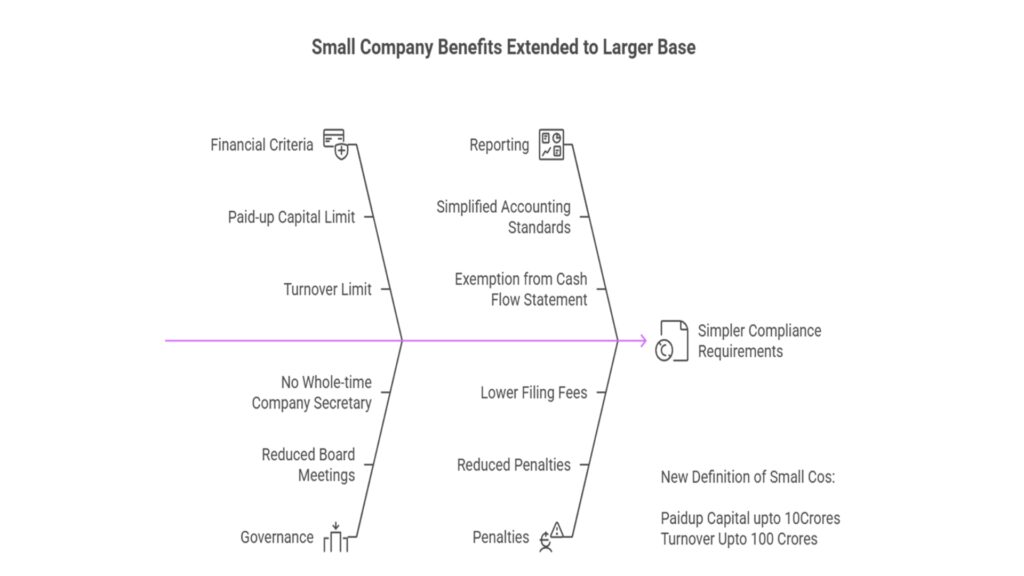

The MCA vide Notification No. G.S.R. 880(E); Dated: 01.12.2025 effective from 1 December 2025 revised the financial criteria used to classify a company as a small company. The definition of a small company now extends to entities with paid-up capital up to ₹10 crore and turnover up to ₹100 crore.

This expansion substantially enlarges the universe of companies eligible for reduced compliance requirements. Small companies form the backbone of India’s entrepreneurial ecosystem, catalysing innovation, employment, and regional economic development.

To promote ease of doing business, the legislative intent has consistently favoured a more facilitative regime for law-abiding entities. The Companies Act, 2013, accordingly provides an extensive suite of exemptions and procedural relaxations specifically tailored for small companies.

Major Reforms - Benefits to Stakeholders

The Companies Act, 2013, accords an array of concessions to small companies, substantially easing their financial and administrative burdens. The following provisions summarizes key benefits:

- Reduced Board Meeting Requirements (Section 173(5)) A small company is deemed compliant if it convenes one Board meeting in each half of the calendar year, with at least a 90-day interval between the two meetings.

- No Requirement of a Whole-time Company Secretary (Section 203(1) r/w Rule 8A) Entities classified as small companies are exempt from appointing a whole-time Company Secretary, reducing fixed overheads.

- Exemption from Internal Audit (Section 138(1) r/w Rule 13) Small companies are not obligated to appoint an internal auditor for evaluating internal controls or operational processes.

- No CSR Committee Requirement (Section 135(1)) CSR provisions do not compel small companies to constitute a CSR Committee or incur mandatory CSR expenditure.

- Applicability of Accounting Standards (Section 133 r/w Rule 4, AS Rules 2021) Small companies comply with the Companies (Accounting Standards) Rules, 2021 rather than Ind AS, simplifying financial reporting.

- Exemption from Preparation of Cash Flow Statement (Section 2(40)) Financial statements may exclude the cash flow statement and related explanatory notes.

- Exemption from IFC Reporting by Auditors (Section 143(3)(i) r/w GSR 464(E) & GSR 583(E)) Auditors are not required to report on internal financial controls for small companies.

- Non-applicability of CARO 2020 (Section 143(11) r/w CARO Para 1(2)(ii)) The Companies (Auditor’s Report) Order, 2020 does not apply to small companies.

- Abridged Annual Return – Form MGT-7A (Section 92(1) r/w Rule 11) Annual return filing is permitted in Form MGT-7A, requiring only director signature unless otherwise mandated.

- No Certification under Form MGT-8 (Section 92(2)) Small companies are exempt from certification by a practicing Company Secretary.

- Abridged Board’s Report (Section 134(3A) r/w Rule 8A) A simplified Board’s Report may be furnished without elaborate disclosures.

- Reduced Statutory Filing Fees (Section 403 r/w Rule 12 & Fee Table) Statutory filing and registration fees are comparatively lower, excluding OPCs.

- No Pre-certification Requirement for Select e-Forms (Section 398 r/w Rule 12(a) & (b)) Several e-forms do not require professional pre-certification.

- Lesser Penalties (Section 446B) Penalties are capped at 50% of prescribed amounts, up to ₹2 lakh for the company and ₹1 lakh for officers in default.

- Exemption from Mandatory Auditor Rotation (Section 139(2) r/w Rule 5) Small companies are relieved from mandatory auditor rotation.

- Eligibility for Fast-Track Merger (Section 233 r/w Rule 25(1A)) Small companies may undertake mergers through the simplified fast-track route.

How to be Prepared

- Entities falling within the revised definition should reassess their compliance frameworks and recalibrate internal policies accordingly. Management should adopt a threshold-monitoring mechanism to ensure ongoing eligibility.

- Governance calendars must reflect the reduced meeting obligations while maintaining a robust documentation trail.

- Financial reporting teams should transition to the appropriate Accounting Standards and remove cash flow statements from annual reporting where permitted.

- Auditors should be formally notified of exemption applicability for CARO, IFC reporting, and auditor rotation requirements.

- Form MGT-7A should be used for annual return filing and adhere to signature norms.

CA Mahipal Sharma | Partner | FCA | CISA | B.Com

Contact: +91 7023030160 | email: mahipal013@gmail.com

Share this article: